Understanding the Benefits of Workers Compensation in Ontario

Getting hurt on the job can turn your world upside down in an instant. Suddenly, you’re not just dealing with pain, but with a tidal wave of worry—about your health, your family, and how you’re going to pay the bills. The benefits of workers compensation are designed to be a lifeline in this exact situation, offering a crucial safety net so you can get support without having to prove your employer was at fault. It’s a system built to help injured workers across Ontario focus on what’s most important: getting better.

Your Financial Safety Net After a Workplace Injury

When an injury happens at work, the physical pain is immediate. But the financial stress isn’t usually far behind. This is precisely why Ontario’s workers’ compensation system was created. Managed by the Workplace Safety and Insurance Board (WSIB), it acts as an essential insurance plan designed to catch you when you fall.

The entire system is built on what’s known as a “no-fault” principle, a cornerstone of Canadian workers’ compensation law. In simple terms, this means you don’t have to wade into a stressful, drawn-out legal battle to prove your employer was negligent just to get the help you need.

Instead, the system is there to provide timely financial and medical support, creating a bridge to help you manage your life while you heal. It’s a recognition that accidents happen, and it puts a structured process in place to support employees from all corners of Ontario, whether they’re on a construction site in Toronto or in an office in Burlington.

The Core Purpose of WSIB

The WSIB’s mission is really two-sided: it works to promote health and safety in the workplace, but it also provides compensation and return-to-work support for those who get hurt. For someone who’s just been injured, its role becomes intensely practical and immediate. It’s set up to address your most urgent needs right after a work-related accident or illness.

Think of it as a specialized support system that handles several key things for you:

- Replacing Lost Income: It provides wage-loss benefits to cover a significant portion of your earnings while you’re unable to work.

- Covering Medical Expenses: It pays for necessary medical care, from physiotherapy and prescriptions to specialized equipment you might need.

- Facilitating Recovery: It helps co-ordinate your treatment and rehabilitation to ensure you can get back to work in a way that’s safe and sustainable.

- Providing Long-Term Support: For workers who suffer a permanent impairment, it offers financial awards to acknowledge the injury’s lasting impact on their life.

A No-Fault System Explained

The “no-fault” aspect is arguably the single biggest benefit of workers compensation in Ontario. Just imagine if, after breaking your leg on a worksite, your only option was to hire a lawyer and sue your employer, trying to prove they were careless. That process could drag on for years, leaving you with no income or medical coverage in the meantime.

The no-fault system removes this massive burden. As long as your injury happened “in the course of” your employment, you are generally entitled to benefits. It doesn’t matter if it was your fault, your employer’s fault, or nobody’s fault. This trade-off is the fundamental deal between workers and employers in Ontario.

In exchange for this guaranteed, no-blame coverage, workers generally give up their right to sue their employer over the injury. This arrangement makes things much more stable and predictable for everyone. Injured workers get help quickly, and employers are shielded from potentially devastating lawsuits. This guide will walk you through how the system works so you can protect your rights and focus on your recovery.

The Core WSIB Benefits That Support Your Recovery

When you’re hurt on the job, your main focus should be on getting better. But it’s hard to do that when you’re worried about medical bills and lost income. That’s exactly why the WSIB system exists.

Think of it as a safety net designed to catch you. It provides a whole suite of benefits to cover everything from your paycheque to your prescriptions. Let’s walk through what you’re entitled to, breaking down the jargon so you know exactly what support is available.

Loss of Earnings (LOE) Benefits

The first question on everyone’s mind is, “How will I pay my bills?” This is where Loss of Earnings (LOE) benefits step in. They are the most immediate and critical form of support, replacing the income you’ve lost because you can’t work.

If your claim is approved, the WSIB pays you 85% of your net average earnings—that’s your take-home pay before you got hurt. They calculate this based on your regular wages, overtime, and any other income to get a fair number. These payments keep coming as long as your injury prevents you from earning your full wages and you’re actively participating in your recovery.

Think of LOE benefits as a financial bridge. It’s designed to keep you stable until you can safely return to work. In cases of severe, permanent disability, these benefits can even continue until you turn 65.

Health Care and Medical Benefits

Your recovery is paramount. The WSIB provides comprehensive health care coverage so you can get the treatment you need without having to pay out of pocket. This benefit is a cornerstone of the system, removing the financial stress that can so often get in the way of proper healing.

This coverage is broad and is meant to cover all reasonable and necessary treatments, including:

- Doctor and Specialist Visits: Any appointments you need to diagnose and treat your workplace injury.

- Physiotherapy and Rehabilitation: Crucial therapies like physio, chiropractic care, and occupational therapy to help you get back on your feet.

- Prescription Medications: The full cost of any drugs prescribed to manage your condition.

- Medical Devices and Equipment: Things like crutches, braces, or specialized tools needed for your recovery are covered.

- Travel Costs: The WSIB can also reimburse you for reasonable travel expenses to get to and from your medical appointments.

To give you a clearer picture, here’s a quick summary of the main benefit types.

A Quick Look at Key WSIB Benefit Categories

| Benefit Category | What It Covers |

|---|---|

| Loss of Earnings (LOE) | Replaces 85% of your net lost income while you can’t work. |

| Health Care | Covers all approved medical treatments, prescriptions, and devices. |

| Non-Economic Loss (NEL) | A one-time payment for the permanent impact of an injury on your life. |

| Survivor Benefits | Financial support for the family of a worker who has passed away from a work injury. |

Each of these benefits plays a unique role in your overall recovery, addressing financial, physical, and long-term needs.

Non-Economic Loss (NEL) Awards

Sometimes, a workplace injury leaves a permanent mark. It could be a lasting physical limitation or a psychological condition that doesn’t fully go away. A Non-Economic Loss (NEL) award is a one-time, lump-sum payment that acknowledges this permanent loss of function.

It’s important to understand that this isn’t about replacing income. Instead, it’s compensation for the non-financial toll of the injury—the pain, suffering, and the impact on your quality of life. The amount is calculated after your doctor determines you’ve reached Maximum Medical Recovery (MMR), which is the point where your condition has stabilized. A specialized medical assessment determines your impairment rating, which then translates into the final award amount.

Survivor Benefits

In the tragic event that a worker dies because of a workplace injury or occupational disease, the WSIB provides critical support to their family. This is a vital safety net for spouses, dependent children, and other dependants facing an unimaginable loss.

These benefits are designed to offer some financial stability during a devastating time and usually include:

- A one-time lump-sum payment for the surviving spouse.

- Ongoing monthly payments for the spouse and any dependent children.

- Coverage for funeral and burial expenses.

- Access to bereavement counselling to help the family cope.

Knowing what you’re entitled to is the first step in protecting yourself and your family. For a more detailed look, you can learn more about WSIB insurance in Ontario in our complete guide. Together, these benefits form a robust system designed to help you navigate one of the most challenging times of your life.

Getting Back to Work Safely and Sustainably

Getting back to work is a huge step in your recovery, but it has to be done right. This isn’t about rushing you back to your old duties before you’re ready. It’s about a return that’s safe, medically sound, and won’t put you at risk of re-injury. That’s precisely why the Workplace Safety and Insurance Board’s (WSIB) return-to-work (RTW) programs are so important.

These programs are one of the core benefits of workers compensation, shifting the focus from just providing a cheque to actively helping you get back on your feet. It’s a team effort—you, your employer, and your WSIB case manager all work together. Your voice and your doctor’s input are central to building a plan that actually works for you.

You can think of your RTW plan like a personalized program from a physiotherapist. It’s a structured, goal-oriented process built around your specific physical or psychological needs, ensuring you don’t push yourself too hard and end up back at square one.

The Team Approach to Your Return

A successful return to work is never a solo mission. In Ontario, the law emphasizes cooperation between you and your employer. This team-based approach keeps everyone on the same page, all aiming for the same goal: getting you back to meaningful work safely.

Here’s how each person fits into the puzzle:

- You (The Worker): Your role is to stay in touch with your employer and the WSIB, go to your medical appointments, and be an active voice in creating and following your RTW plan.

- Your Employer: Legally, your employer must try to modify your job or workplace to accommodate your needs, unless doing so would cause them undue hardship.

- The WSIB: The WSIB acts as the facilitator. They bring in specialists and provide resources to help design and monitor the RTW plan, making sure it lines up perfectly with your medical restrictions.

This collaborative structure helps avoid confusion and ensures any plan is based on clear, current medical advice about what you can and can’t do safely.

The ultimate goal of an RTW plan is an Early and Safe Return to Work. This means finding suitable work that fits your functional abilities, respects your recovery, and helps you rejoin the workforce as soon as it’s medically appropriate.

Practical Tools for a Safe Return

The WSIB has several practical tools at its disposal to build a custom RTW plan just for you. These aren’t just about getting you back on the clock; they’re about making sure your return is sustainable and doesn’t jeopardize your health.

Modified Work Plans

One of the most common approaches is a modified work plan. This doesn’t automatically mean a completely new job. More often, it’s about tweaking your old role to fit within your current limitations.

Examples of modified work could be:

- Working fewer hours or taking more frequent breaks to manage fatigue.

- Changing physical tasks, like avoiding heavy lifting or not standing for long periods.

- Shifting your duties to focus on tasks that won’t aggravate your injury.

If you’re dealing with lingering issues from your injury, learning how to relieve chronic back pain with practical strategies can be a game-changer for your recovery. This knowledge also helps you better communicate your needs when building that modified work plan.

Workplace Accommodations

Sometimes, the work environment itself needs to change. These adjustments are called accommodations, and your employer is required to provide them. They can be simple, like getting a new ergonomic chair or a height-adjustable desk, or more complex, like specialized computer equipment to reduce strain.

Ultimately, these programs show how the benefits of workers compensation go beyond financial aid. They create a structured path back to work that protects your health and honours your recovery. It’s also important to remember that psychological injuries need the same kind of support; you can read more on this in our article about mental health leave in Ontario. This system is designed to make sure your return to work is a positive step forward, not a setback.

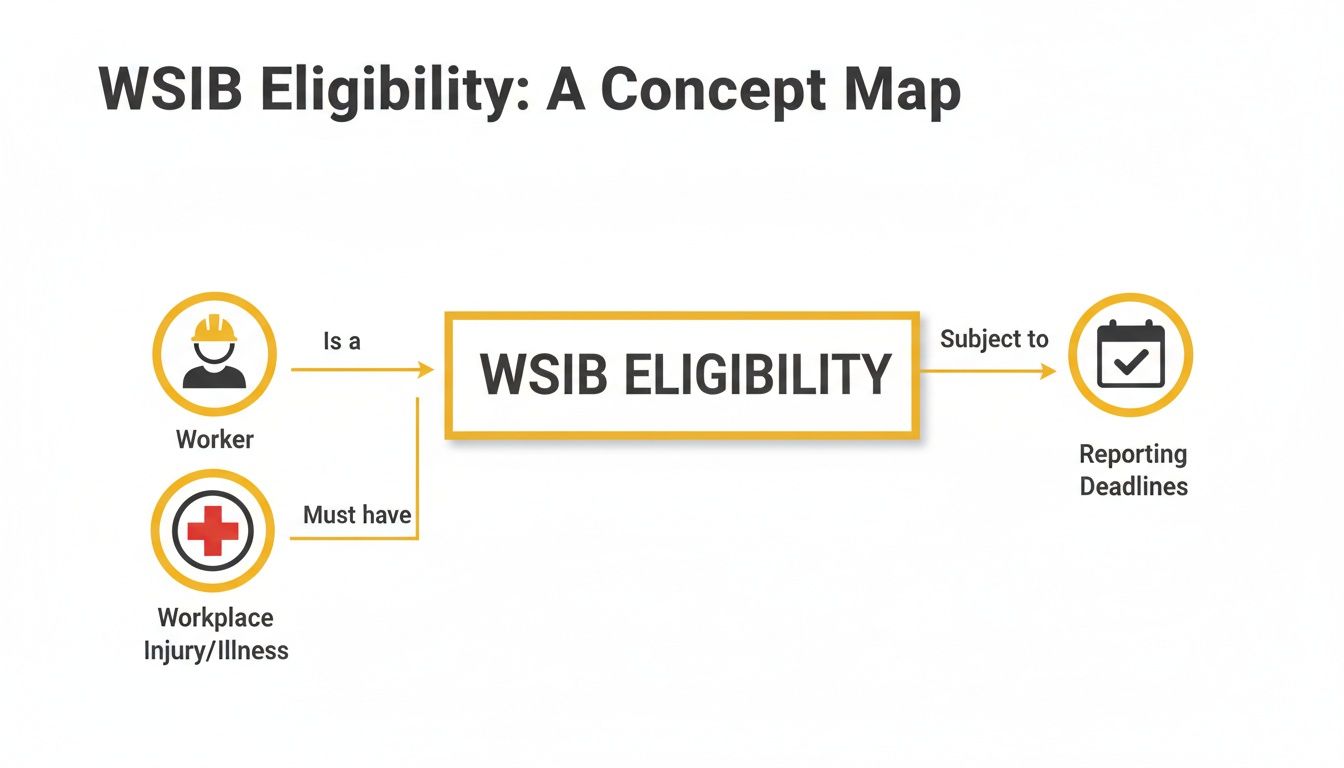

Navigating WSIB Eligibility and Critical Deadlines

When you’re hurt at work, getting the support you need from workers’ compensation comes down to two things: being eligible and filing on time. Think of it like a train ticket—you need to be the right passenger for that train, and you need to get on board before it leaves the station. Miss either of those, and you’re left on the platform.

It’s a straightforward concept, but the rules can feel complicated. Let’s cut through the jargon and get right to what you need to know about who qualifies as a ‘worker’, what counts as a ‘work-related’ injury, and the critical deadlines you can’t afford to miss.

Who Is Covered by WSIB in Ontario?

The good news is that Ontario’s Workplace Safety and Insurance Act casts a wide net. The system is designed to protect most employees across the province, whether you’re working in a bustling Toronto office or on a remote construction site up north.

So, who is considered a ‘worker’? Generally, if your employer is legally required to have WSIB coverage, you’re covered. This isn’t just for the 9-to-5 crowd; it includes:

- Full-time, part-time, and casual employees

- Staff hired through temporary agencies

- Seasonal workers and apprentices

- Even some independent contractors, depending on how integrated they are into the business

It’s important to know that some industries aren’t automatically covered, like banks or private healthcare practices, though they can opt in. If you’re not sure about your employer, the WSIB has online tools to check their coverage status.

Defining a Work-Related Injury or Illness

For a claim to be successful, your injury or illness must “arise out of and in the course of employment.” That’s the key legal phrase, and it simply means your work activities have to be linked to your medical condition.

This goes far beyond a sudden slip and fall. The definition is broad and includes:

- Occupational Diseases: These are conditions that sneak up on you over time because of your work environment. Think of a factory worker developing hearing loss from years of loud machinery or a miner contracting a lung disease.

- Repetitive Strain Injuries: Carpal tunnel from typing or tendonitis from repeated lifting are classic examples of injuries caused by doing the same motion day in and day out.

- Psychological Trauma: Mental health is health. Conditions like PTSD that stem from a specific shocking event at work or from a sustained pattern of workplace harassment can also be covered.

Remember, the injury doesn’t have to happen on company property. If you’re a salesperson who gets into a car accident while driving to a client meeting, that’s still considered a work-related incident and is eligible for WSIB benefits.

The Two Most Important Deadlines in Your Claim

After you’ve been hurt, the clock starts ticking. The WSIB enforces strict deadlines, and missing them can jeopardize your entire claim, sometimes to the point of outright denial.

Here are the two timelines you absolutely must respect:

-

Report to Your Employer Immediately: Your first duty is to let your employer know you’ve been injured. Do it as soon as it happens or as soon as you realize your condition is connected to your job. Prompt reporting is always your best move.

-

File Your Claim with the WSIB Within Six Months: This is the big one. You have a hard deadline of six months from the date of injury to file your official claim (a Form 6) with the WSIB. If it’s an occupational disease that developed slowly, the clock starts ticking from the day you learned the illness was work-related.

These aren’t flexible guidelines—they’re firm rules. It’s always better to report an injury and start a claim, even if it seems minor at first. Some injuries get worse over time. For more insight into how these time limits work across different areas of law, our guide on the statute of limitations in Canada provides a helpful overview. Taking these first steps correctly is the most powerful thing you can do to protect your right to compensation.

How WSIB Interacts with Other Disability Benefits

If you’ve been hurt at work, you’ve probably realized that your WSIB claim is just one piece of a much larger puzzle. Many people in Ontario also have access to other safety nets, like private Long-Term Disability (LTD) insurance from their employer or Canada Pension Plan (CPP) Disability benefits. Figuring out how all these systems work together is absolutely critical to keeping your finances stable while you recover.

It’s not as simple as collecting three separate cheques. The entire system is built to prevent what’s called “double-dipping”—making sure you don’t receive more than 100% of your pre-injury income. This is done through a process known as offsetting, where one benefit payment reduces the amount you get from another.

Think of it like a pecking order. There’s a clear hierarchy for who pays first, and getting the order wrong can lead to some serious headaches—payment delays, confusion, and even demands to pay back thousands of dollars in overpayments.

The journey starts with a valid WSIB claim, which has its own specific requirements.

As this shows, it all begins with a worker suffering a work-related injury or illness, and then following the strict reporting deadlines to even get in the door.

WSIB Is The “First Payer”

Here’s the golden rule in Ontario: if your injury or illness happened because of your job, WSIB is almost always the first payer. This means the WSIB has the primary responsibility to cover your lost wages and medical bills.

Because of this, most private LTD insurance policies have a clause that says they won’t pay for a disability that’s already covered by workers’ compensation. If you try to claim LTD for a workplace injury, your insurer will almost certainly tell you to file with the WSIB first. They’ll then sit on your application and wait to see what the WSIB decides.

Key Takeaway: For any injury that happens on the job, your first port of call is the WSIB. Your LTD insurer views the WSIB as the primary source of funding and will adjust—or deny—their payments based on what WSIB provides.

How LTD and CPP Disability Benefits Are “Offset”

So what happens if your WSIB benefits don’t fully cover what your LTD plan would have paid? In that case, your LTD insurer might pay a “top-up” amount. But—and this is a big but—they will deduct your WSIB payments, dollar-for-dollar, from what they owe you under the policy.

Here’s a simple example:

- Your monthly LTD benefit is $3,000.

- Your monthly WSIB payment is $2,500.

- Your LTD insurer will offset the WSIB amount and pay you the difference: $500.

CPP Disability benefits are treated the same way. Both WSIB and most LTD policies have the right to offset any CPP Disability benefits you get. So, if you’re approved for CPP Disability, your WSIB or LTD payments will likely be reduced. To get a better handle on the fine print in these private plans, you can learn more about how Long-Term Disability insurance policies work.

Let’s break down how these three pillars of support interact when you’re dealing with a workplace injury.

Coordinating WSIB, LTD, and CPP Disability Benefits

| Benefit Source | Primary Role in a Workplace Injury | How It Interacts with Other Benefits |

|---|---|---|

| WSIB | This is the first payer. It covers wage loss and medical care for work-related injuries and illnesses. | WSIB payments reduce (or offset) the amount you can receive from most private LTD insurance policies. |

| LTD Insurance | Acts as a secondary payer or “top-up” if WSIB benefits are less than your full LTD entitlement. | LTD benefits are reduced dollar-for-dollar by any WSIB payments you receive. They are also often reduced by any CPP Disability benefits. |

| CPP Disability | Provides a basic income replacement for those with a “severe and prolonged” disability that prevents them from working. | Both WSIB and LTD insurers typically have the right to reduce their payments by the amount you receive from CPP Disability. |

Understanding these relationships is not just about paperwork; it’s about protecting your financial future. Making sure every claim is co-ordinated correctly ensures you get the maximum support you’re entitled to without running into trouble later on.

What to Do When Your WSIB Claim Is Denied

Getting a denial letter from the Workplace Safety and Insurance Board (WSIB) is crushing. After everything you’ve been through with your injury, seeing your claim rejected can feel like hitting a brick wall. But it’s so important to know this: a denial is not the end of the line.

Far from it. A denial is simply the starting point of the formal appeals process. You have the right to challenge the decision, and this is your chance to set the record straight.

Understanding the Appeals Process

The WSIB appeals system in Ontario has two key levels. Your first move is to appeal the decision to the WSIB’s own Appeals Branch. Here, your file gets a fresh look from an Appeals Resolution Officer (ARO), a specialized decision-maker who has the power to reverse the original denial.

Think of the ARO as a new set of eyes. They will review all the evidence—the old and the new—to see if the first decision was fair and correct. Many claims get approved at this stage, often because the injured worker provides stronger medical evidence or clearer details that were missing the first time around.

If the ARO doesn’t rule in your favour, you still have one more shot. The final step is taking your case to the Workplace Safety and Insurance Appeals Tribunal (WSIAT).

WSIAT is a completely independent body, separate from the WSIB. It functions like the final court for workers’ compensation in Ontario. Its decisions are binding, making this your last and most formal opportunity to argue your case.

Building a Stronger Case for Your Appeal

A winning appeal is built on strong evidence. The good news is that the denial letter itself gives you a roadmap—it will tell you exactly why your claim was rejected. Your job is to tackle those reasons head-on with solid proof.

Here are some of the most common reasons claims get denied:

- Insufficient Medical Evidence: The WSIB might think your doctor’s report didn’t firmly connect your injury to your work tasks.

- Missed Deadlines: Failing to report your injury or file your claim within the strict six-month time limit is an automatic red flag for the WSIB.

- Pre-Existing Conditions: The Board might argue that an old injury or underlying condition is the real cause of your current disability, not your work.

- Disputes Over the Incident: Sometimes, an employer gives a different account of what happened, which creates doubt about how you were actually injured.

To overcome these roadblocks, you need to gather better, more persuasive evidence. This could mean asking your doctor or a specialist for a more detailed medical opinion, getting written statements from co-workers who saw what happened, or even finding an expert to weigh in. For very complex situations, learning how a workplace injury lawsuit is structured can give you insight into the kind of proof needed to win.

If you’re facing a denial, getting legal help can make all the difference. Understanding how a retainer for a lawyer works is a good first step in preparing for that process. With a strategic, well-supported appeal, you can turn that denial into an approval and get the benefits you deserve.

Your Top Questions About Ontario Workers’ Compensation

Trying to figure out the workers’ compensation system can feel like learning a new language, especially when you’re hurt and stressed. It’s completely normal to have a lot of questions. To help clear things up, we’ve put together straightforward answers to the questions we hear most often from injured workers across Ontario, from Burlington to the greater GTA.

Knowing your rights is the first and most important step in making sure you’re protected while you focus on getting better.

Can I Choose My Own Doctor for a WSIB Claim?

Yes, absolutely. The choice is yours. In Ontario, you have the right to see your own family doctor or any other healthcare professional you trust. Your employer cannot force you to see a specific doctor they’ve chosen for your work-related injury.

The key thing to remember is to tell your doctor that your injury happened at work. This is crucial because it signals to them that they need to fill out the right WSIB paperwork, like the Health Professional’s Report (Form 8). This form is a cornerstone of the medical evidence for your claim.

What if My Employer Tells Me Not to File a Claim?

That’s a major red flag. It is against the law for any employer in Ontario to try to talk you out of filing a WSIB claim or to penalize you in any way for getting injured. This illegal practice is known as “claim suppression,” and it’s a serious offence. Your right to benefits is granted by law, not by your employer’s approval.

If you’re feeling any pressure from your employer to keep your injury quiet, you should bypass them and file your claim directly with the WSIB. Your health and your rights come first. The WSIB is the only one who decides if you’re eligible for benefits, not your boss.

How Long Do WSIB Wage Loss Benefits Last?

This is a common worry, but there’s no single, fixed timeline. Loss of Earnings (LOE) benefits are designed to last as long as you’re losing income because of your work injury and are actively participating in your recovery and return-to-work plans.

Generally, these benefits continue until one of these things happens:

- You’ve recovered from your work-related injury.

- You are no longer losing wages (for example, you’re back to your regular job and pay).

- You turn 65 years old.

If a worker suffers a severe, permanent injury that makes it impossible to ever return to any kind of employment, benefits can potentially continue right up until age 65.

Do I Have to Accept a Modified Job Offer?

You do have a responsibility to co-operate with your employer’s efforts to get you back to work safely. If your employer offers you a suitable modified job that fits perfectly within the medical restrictions laid out by your doctor, you are generally expected to accept it.

Turning down a genuinely suitable offer without a good reason can cause the WSIB to suspend your benefits. However—and this is important—if you truly feel the job is unsafe or asks you to do more than your doctor has cleared you for, you need to speak up immediately. Let both your employer and your WSIB case manager know about your concerns right away.

Navigating a WSIB claim can be a tough road, but you don’t have to walk it alone. If your claim has been denied or you just need some guidance on your rights, the team at UL Lawyers is ready to help. Get in touch with us for a free consultation to make sure you get every single benefit you’re entitled to. Learn more at https://ullaw.ca.

Related Resources

Your Guide to Hiring a Workplace Injury Lawyer in Ontario

Continue reading Your Guide to Hiring a Workplace Injury Lawyer in OntarioNEED A LAWYER?

We are here 24/7 to address your case. You can speak with a lawyer to request a consultation.

905-744-8888GET STARTED WITH A FREE CONSULTATION

Why Choose UL Lawyers

- Decades of combined experience

- Millions recovered for our clients

- No fee unless we win your case

- 24/7 client support

- Personalized legal strategies